UPS Access Points allow package pickup at stores

The holiday shopping season offers thieves a greater opportunity to snatch those parcels left at the front door.

Source: 6abc.com

The holiday shopping season offers thieves a greater opportunity to snatch those parcels left at the front door.

Source: 6abc.com

A new version of KioWare Classic for Window is now available. The KioWare Classic for Windows Products (available in Lite, Basic, and Full), act as a secure kiosk mode, locking down the Windows operating system and desktop. Version 7.4.0 of KioWare Classic Lite, KioWare Classic Basic and KioWare Classic Full provides customers of the original KioWare software with… Read More »

Consumer experiences, particularly those with uncomplicated digital transactions such as Uber and AirBnB, are frequently being compared to and referenced in unrelated industries. The ease and simplicity of these platforms raises the question: ‘Why can’t all customer service and payment transactions be this easy?’

Source: www.cmo.com.au

As digital disruption and technological innovation elevate the competitive stakes, companies are quickly learning they must adapt to rapidly changing consumer behaviour or risk drowning in this new liquidity.

Take Coca-Cola Amatil’s retrofitting of vending machines. The beverage company boosted sales by up to 12 per cent after creating a fresh and personalised vending experience through the installation of touchscreens, video cameras and Microsoft Kinect technology. The marketing team borrowed tactics traditionally employed by technology and audiovisual offerings to sell a consumer packaged good.

Not only did the improvement of the vending machines drive sales, the data created by these connected apparatus is enabling Cola-Cola Amatil to make better decisions about cooler placement, restocking, and wider retail needs.

As the marketing and business focus of leading brands shifts from the competitor to the consumer, brands should consider three critical elements in order to position themselves for success in a ‘liquid’ environment:

Get personal

As people increasingly compare their experiences and develop ‘liquid expectations,’ the erosion of consumer loyalty has been recorded. A global study conducted in 2014 by Accenture found six in 10 respondents were more likely to switch from one provider to another compared to 10 years ago. Of that group, 50 per cent said they would consider future offers from non-traditional players that they may never have previously considered.

Read rest of article

Retail stores meld digital experiences into physical shopping to remain relevant. Including Selfie Sweepstakes

Source: www.azcentral.com

Retailers across the board are merging digital connectivity with physical stores. For example, Walmart reports that more than 25 million customers used online store maps and ads to plan their Black Friday excursions to stores across the country.

The merging of digital and physical shopping is seen at high-end stores as well. For example, Origins, a skin-care retailer, spent 10 weeks remodeling its Biltmore Fashion Park location ahead of the holidays to make it more interactive.

Shoppers can choose from one of five free “mini-facial” treatments when they visit the store, and a sample wall is lined with candy jar-like dishes of product for them to test.

Focusing on the in-person experience doesn’t mean the company shuns the Internet. In addition to its online sales, the company has an Instagram social-media campaign for customers to post pictures of themselves wearing facial masks, a core product.

The #maskmonday promotion gives loyal (and unreserved) customers the opportunity to win free masks by posting photos of themselves and tagging the store.

“It’s really popular,” Hatcher said.

The mall also has a promotion through Dec. 20 in which shoppers who take a “selfie” with any of the holiday décor and post it on Facebook or Instagram can win a hotel and ice-skating package at the Hotel Palomar in downtown Phoenix (using the skating rink from fellow RED property CityScape).

At RED’s Aspen Place Shopping Center in Flagstaff, anchored by an REI store, there will be a similar selfie sweepstakes, Jones said.

Costco stock is on the rise after a strong November led to analysts declaring the company ‘Amazon-proof.’

Source: www.businessinsider.com

Becoming “Amazon-proof” is an enviable position for any retailer, as the company’s online dominance has most major retailers such as Target and Walmart playing catch-up.

But Costco has been able to hold its own because of its membership model and ability to incentivize visits to brick-and-mortar locations.

Membership programs are on the rise, with services such as Amazon Prime and online-grocery startups quickly growing. While there are newcomers in the membership area, Costco’s 44.6 million households is an enormous number, accounting for $785 million in sales in the fourth quarter.

Amazon has a new brick-and-mortar bookstore in Seattle. It’s like every other bookstore, save for one really annoying feature.

Source: www.businessinsider.com

Where is ESL technology when you could use it. Reminds us of Costco and their catalog (no prices).

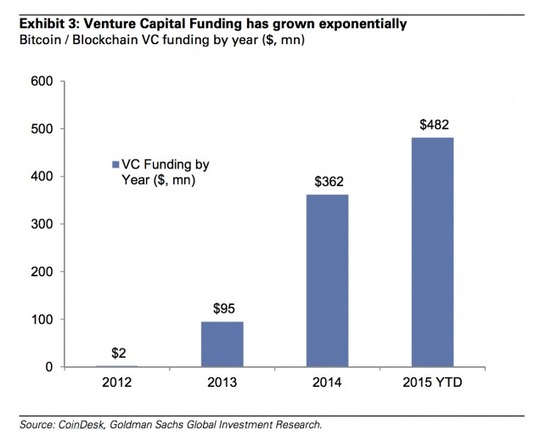

Goldman Sachs notes in a research note sent to clients today, that bitcoin might just be the “opening act” for blockchain technology.

Source: www.coindesk.com

One big draw for GS is that time to close and transaction costs for that will be greatly reduced. Collecting money will be quicker and sometimes people only have the cash for the moment. Get it while it is there now is GS tactic.

Malware designed for POS insertion is getting only more dangerous. Plus tablets being infected at time of manufacture. The cyber criminals never sleep.

Source: www.theexaminer.com

This new ModPOS malware has taken advantage of a flaw in the internal in-store processing of debit and credit transactions still using magnetic stripes as well as using the new EMV Chip and Pin cards; the processing flaw, now known to the retail industry, is that the internal processing systems utilized by many major retailers does not support end-to-end encryption, and does not also properly encrypt data in memory, allowing that data to be captured and sent to distant cyber crooks. According to iSIGHT, “Criminals can then reuse card data, even from EMV cards, to make online (card-not-present) transactions.”

Source: www.linkedin.com

International card schemes MasterCard and Visa now account for 86% of all payment cards in Europe, as domestic and private label schemes continue their decline. RBR’s study Global Payment Cards Data and Forecasts to 2020 shows that €9 out of €10 spent using a payment card in Europe was made on a Visa or MasterCard-branded card – the highest share of any region.

There were 1.5 billion payment cards in circulation in Europe at the end of 2014 which were used for payments worth €2.9 trillion during the year. Competition between the two leading schemes is fierce, with very little difference between Visa and MasterCard in terms of card numbers. With regard to payment value, however, Visa is by far the larger scheme, and gained a percentage point of value share in 2014, while MasterCard lost a percentage point.

Automated retail is a self-service category in the form of standalone machines located in high-traffic areas such as airports and malls and convenient stores. In an era of growing mobility, the consumers demand easy access to products and services anytime…

Source: empowerednews.net